Interesting housing market tidbits from the past week. Housing affordability/inventory shortages/inflationary pressures all remain key themes, both directly and indirectly impacted by the current rate environment.

- “We’re looking at a moment in time where on the one hand, there is a supply shortage. But on the other hand, the consumer out of the necessity is looking for elements of incentives or discounts to be able to afford … the housing stock that they need.”

- “If the Fed is actually going to begin to cut rates, we believe the pent-up demand will be activated.”

- Source: Stuart Miller: Chairman/CEO Lennar Homes

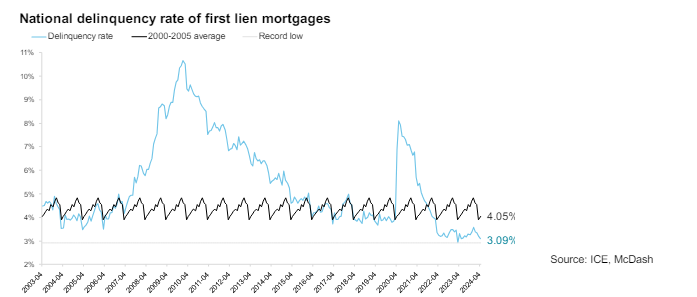

- The national delinquency rate fell to 3.09% in April – its second lowest level on record behind only March ’s record low of 2.92% – marking a 22-bps improvement from the same time last year.

- Source: ICE Mortgage Monitor Report June 2024

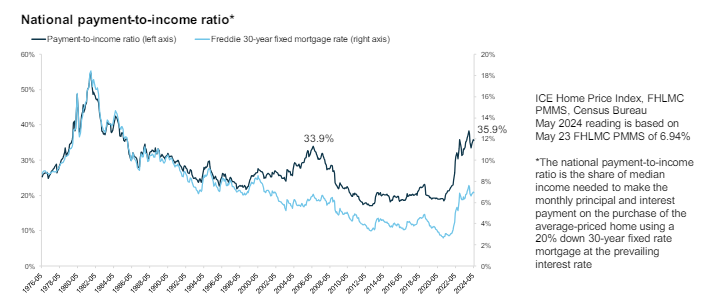

- Home affordability saw marginal – and ultimately momentary – improvement in May

- As of May 23, with 30-year rates at 6.94% according to Freddie Mac PMMS, it required 35.7% of the median household income to afford the median-priced home, some 11.4 percentage points above the 30-year average

- All the nation’s largest markets currently remain less affordable than their long run averages

- With higher interest rates and reduced demand this spring, 90% of major markets are seeing more homes for sale than there were at this same time last year

- Home price growth cooled for the second straight month in April as elevated interest rates resulted in softer demand and improved inventory

- The annual home price growth rate cooled to 5.1% from a revised 5.7% in March, and as high as 6.1 % back in February

- With supply still 36% short and purchase mortgage demand 45% below pre-pandemic levels in recent weeks, shifting 30-year rates in either direction could serve to heat or cool the market relatively quickly.