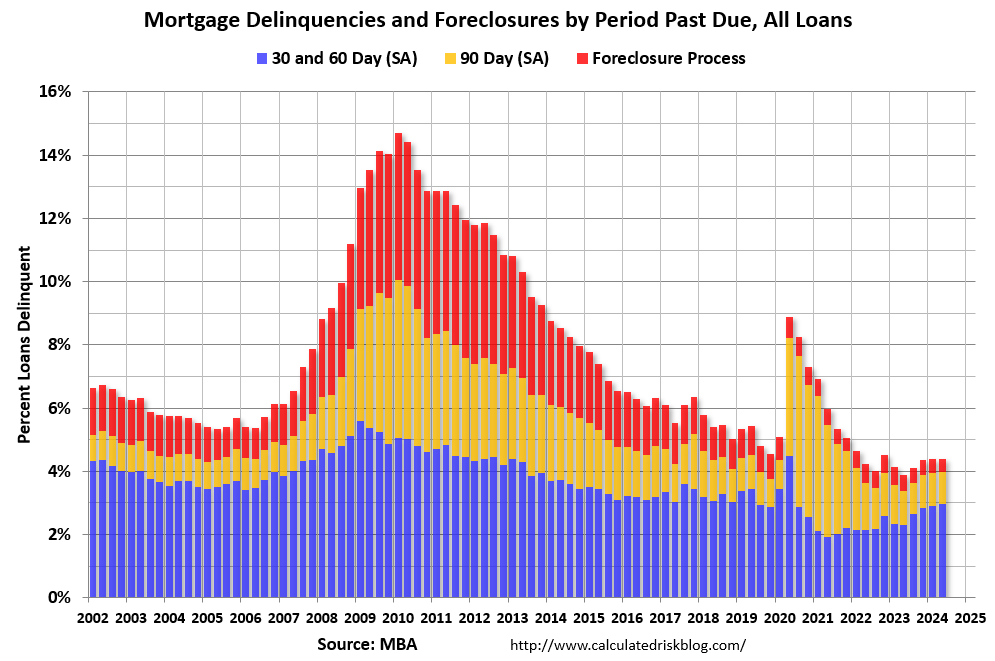

This article provides a good summary of the stability most homeowners currently have in their housing situation. The key line is: “With substantial equity and low mortgage rates (mostly fixed rates), few homeowners will face financial difficulties.”

This graph effectively illustrates how, compared to the housing crisis, most homeowners are in a strong position.

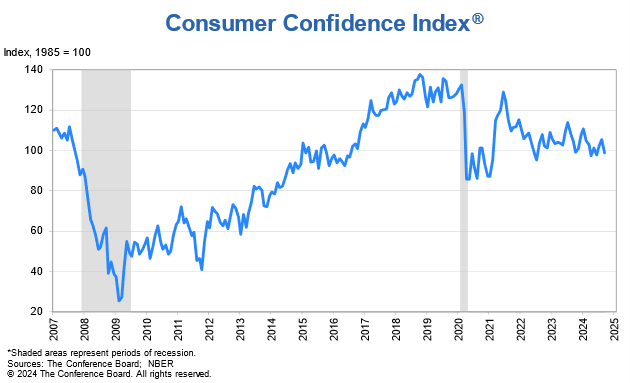

Stable housing should have a significant impact on how people perceive their financial situation, so I reviewed the latest consumer confidence data:

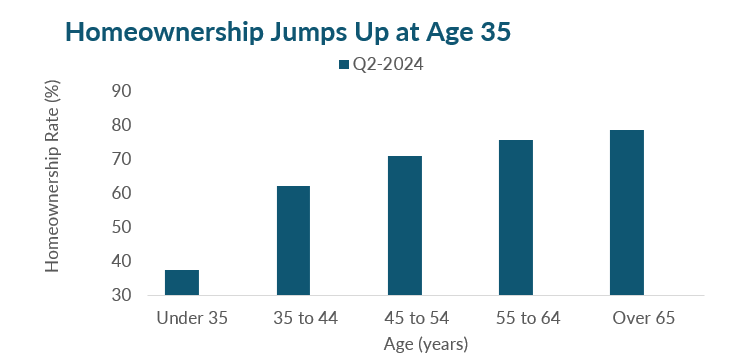

The article’s comments pointed out that “The drop in confidence was steepest for consumers aged 35 to 54. As a result, on a six-month moving average basis, the 35–54 age group has become the least confident, while consumers under 35 remain the most confident.” This is notable, given the homeownership rate is 38% for those under 35 and north of 60% for older age groups.

When comparing the two graphs, it’s apparent that the delinquency rate is on the rise, matching the drop in confidence. While there are other factors contributing to declining consumer confidence (such as inflation and unemployment), housing remains a significant component of how people perceive their current economic stability.

My takeaway from this analysis is that although the delinquency rate is still low compared to the housing crisis—meaning we shouldn’t fear a massive wave of foreclosures—there’s a more pressing concern: rising unaffordability. It’s not a crisis yet, but with delinquencies ticking up and consumers signaling awareness through falling confidence, this trend definitely bears watching.